The cost of borrowing is important to us all. While the physical price of a big ticket item is important, it doesn’t reflect what many of us actually has to pay for it.

Take the cost of a car, for example. The average price paid for a motor in the UK is said to be £21,164. Not many of us has that sort of cash lying around – or indeed the money needed to buy a more modest model either.

Most of us would need to pop some numbers into a loan calculator and work out what that would end up costing by the time we’ve paid it back.

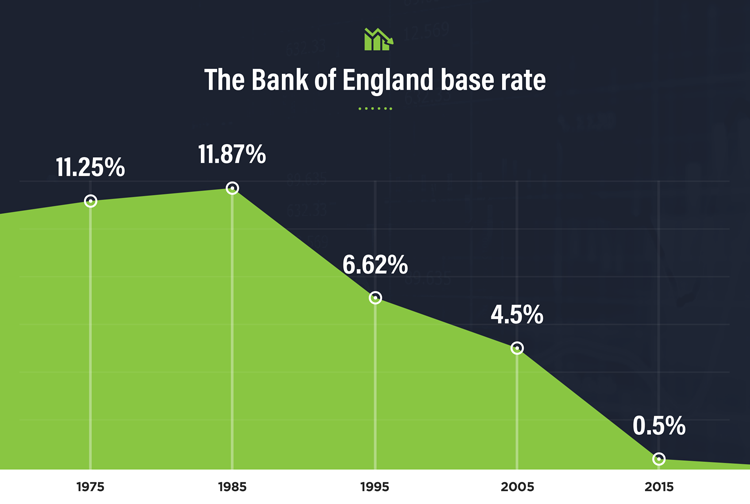

That’s why the interest rate is important. Data from the last few decades shows how much this has fallen. In 1975, the Bank of England base rate was 11.25%. By 1995 that had almost halved and by 2015 is had fallen to 0.5%. It now sits at just 0.25%.

These numbers don’t reflect the cost we actually pay when borrowing, but they are closely linked to the offers we can get.

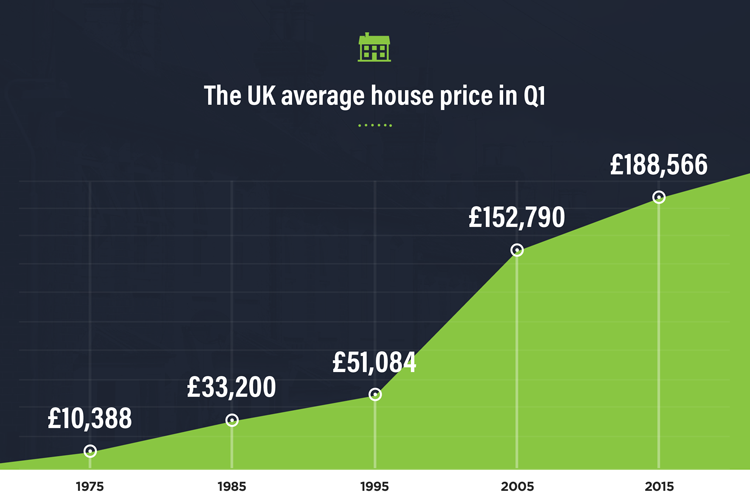

So, while the cost of everything might have gone up over the past 40 years – at least we don’t have to pay more for the privilege of loaning money from a bank. It might be a fairly small silver lining, but while the cost of a car is 11.5 times more than it was in 1975, houses 18 times more and even a pint of beer 20 times the price of ’75, it’s a much needed positive.

Experts also reckon the cost of borrowing should stay low for a while yet, with the Bank of England rate tipped to be below 0.5% until 2021.